![]()

Dear Investors and Partners,

Global financial markets have been experiencing a “slight turbulence,” although markets appear to be stabilizing in recent days, the latest employment report published by the U.S. Bureau of Labor Statistics suggests that it is uncertain whether we have returned to “smooth sailing,” and markets may remain volatile for another short period of time. According to the Jobs Report, the U.S. economy suffered an unexpected setback in July as hiring fell sharply and the unemployment rate rose for the fourth consecutive month, compounded by the rate hikes that have taken a toll on businesses and households. Employers added just 114,000 jobs in July — 35% fewer than expected — and unemployment, now at 4.3%, is the highest since October 2021. Many believe that the root cause of this sharp decline in hiring and economy slowing down is due to the Federal Reserve waiting too long to cut interest rates. Companies are reporting that instead of hiring more, they are using their funds to pay interests on their business loans, which have become a very heavy burden to them in the past year.

Usually, our monthly reviews focus on the real estate and mortgage markets. The reason I chose to open this review with a reference to the recently published July employment report is that this report may best reflect the state of the U.S. economy and, ultimately, affects various sectors of the economy, including the real estate market. Much ink has been spilled by economists and experts over the past year about when and what would trigger the Federal Reserve to begin lowering interest rates. I believe that following this report, together with the positive downward trend on the CPI showing that inflation is cooling, there seems to good reason to believe that there will be a rate cut. This Jobs Report has led many on Wall Street to believe that the Fed will cut rates more deeply in September than they had previously expected, and continue with more cuts throughout 2024.

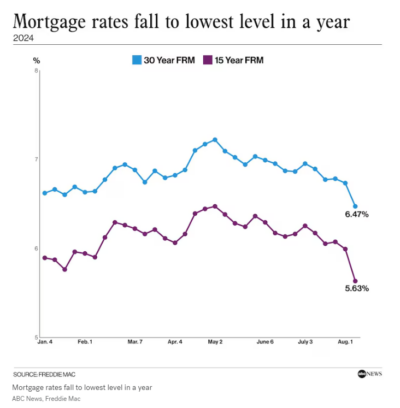

These expectations of a Fed rate cut are already reflected in mortgage rates, which continue to drop and are currently at their lowest levels since May 2023. The interest rate on the 30-year mortgage is now 6.47%, and the fixed rate for a 15-year mortgage has fallen below the 6% threshold to 5.63%. Just last month, the interest rate for a 30-year mortgage fell below 7% (at 6.95%), and we have seen it continue to drop another half a of a percent, with the 15-year mortgage rate dropping even more sharply.

The natural progression of the market, based on the expected Fed rate cut and significantly lower mortgage rates, leads to an increase in mortgage applications for refinancing home loans. Applications to refinance these loans, which are highly sensitive to interest rate changes, surged by 16% this week and are about 60% higher compared to the same week last year. The drop in mortgage rates increases the purchasing power of potential homebuyers and should begin to pique their interest in making a move. Yet, we have not seen a significant pick-up in applications for mortgages to purchase homes, increasing by a mere 1%. Despite the optimism in the market, both home prices and borrowing rates remain high which makes purchasing a home unattainable for many.

One of the trends which we follow which has shifted and is likely due to the lower mortgage rates is the increase in the number of contracts signed for new home purchases in Manhattan and Brooklyn. Contracts signed in Manhattan for new apartments increased by 40.1% year-over-year, and in Brooklyn, by 30.6% year-over-year. New signed contracts for residential buildings with 1-3 units in Brooklyn rose by 122.7% compared to July of the previous year! These figures indicate that a rise in demand for new mortgages is likely in the coming months (typically the buyer has 30-60 days to secure the necessary financing for the purchase). These statistics are of course very positive for the market and for us suggesting that more activity is expected in the market in which Golden Bridge operates, along with other new opportunities.

Additional signs of market recovery and trends shifting can be found in the heart of the global real estate capital—Manhattan. The residential real estate market there has recently shifted to a “buyers’ market.” Apartment prices in Manhattan are declining as a result of increased inventory breeding competition that makes it longer to sell a home. The average real estate sales price in Manhattan fell 3% to just more than $2 million. Currently there are now more than 8,000 apartments for sale in Manhattan, which is higher than the 10-year average of about 7,000 according to the Miller Samuel appraisal firm. With the gap narrowing between buyer and seller expectations, more deals are closing. There were 2,609 residential sales in the second quarter, up 12% from a year ago marking the first sales rebound in two years.

The year 2024 has presented significant challenges due to enduring high interest rates, impacting those with loans and mortgages. While many anticipated reductions in interest rates, concerns from the Fed about potential inflation have kept rates stable. This persistent pressure affects both borrowers and lenders, with many borrowers struggling to meet high interest demands, banks reluctant to refinance, and lenders seeing an increase in non-performing loans.

At Golden Bridge, we’ve felt the market’s impact and prepared by enhancing our borrower monitoring and management strategies. Our approach involves managing the entire loan lifecycle in-house—from due diligence and origination to servicing—allowing us to closely connect with our borrowers and swiftly address issues, offering customized solutions or pursuing legal action if necessary.

Our monthly reports throughout the past year have detailed our initiative to reduce the fund’s loan-to-value (LTV) ratio, which currently stands below 50%. With eight years of experience and numerous resolved credit events, we have recognized the critical role of maintaining a low LTV, in addition to securing first liens and personal guarantees, in protecting our investments and avoiding losses.

Despite current challenges, our proactive strategies have proven effective, and I believe these times offer unique opportunities for Golden Bridge’s investors. We anticipate that upcoming rate cuts in the US could further enhance these prospects.

Erez Britt, Founder and CEO

See below links to Golden Bridge fund fact sheets:

- Example of loan:

Address: ROUTE 9W PALISADES, NY

Last month Golden Bridge secured a $15,000,000 loan with a first position lien security interest towards a convention center campus just north of New York City. This campus which was originally built by IBM as its own conference and training facility is built on 106 acres, and currently includes 206 guest rooms, 43 conference rooms, a 48,000 sqft event hall, fitness center, indoor pool, basketball volleyball and tennis courts walking trails and bar & lounges. Additionally, the previous owner applied to the township to build 342 townhouses and apartments on the property. After significant due diligence on our borrower and on the property we structured the loan and accompanying fees to best maximize the return for our investors.

Loan Amount: $ 15,000,000

Property Value (As Is): $ 31,500,000

LTV As Is (loan to property value ratio): 48%

Loan Duration: 12 Months

Reminder that it is possible to see the fund’s loans on New York City’s website:

https://a836-acris.nyc.gov/DS/DocumentsSearch/PartyName

(Business party name: Golden Bridge)

For additional information, don’t hesitate to contact us.