![]()

Dear Investors and Partners,

I am delighted to begin by highlighting a significant milestone for Golden Bridge, even though we marked it internally a few months ago. Among all the many tasks and continuous daily activities to enhance our portfolio, this achievement has yet to be shared with our investors.

As I mentioned previously, when we launched the Golden Bridge Fund nearly eight years ago, we recognized the need for an investment solution like the one the fund offers—one that would cater specifically to investors in Israel. From the outset, we set ourselves an ambitious goal: to continuously break records. However, to be honest, we never expected that, within just eight years, the fund would reach another remarkable milestone: over a billion dollars in credit issued since its inception! This debt has been originated towards 569 distinct loans, of which 440 have already been repaid in full. Throughout these eight years, the fund and its investors have successfully navigated various investment cycles, a global pandemic, and significant geopolitical challenges. Despite these complexities, we have consistently identified the best opportunities, delivering strong returns for our investors. We are committed to continuing this journey and are excited to break even more records with you in the years to come!

At the beginning of the month, we learned of the election of a new (or rather, old) president to the White House. Donald Trump will once again assume the role of president of the world’s largest economy beginning in January 2025. Immediately following the announcement of his victory, the impact on U.S. real estate markets became evident.

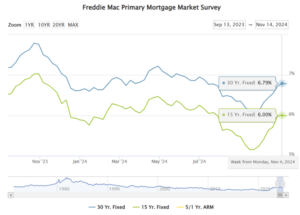

As we discussed in our previous update, mortgage rates—particularly the 30-year and 15-year fixed rates—are closely tied to the yields on 10-year Treasury bonds. In the wake of Trump’s election, government bond yields continued to climb, and, as a result, the average 30-year mortgage rate surged to 6.79%. Similarly, 15-year mortgage rates have risen back to 6%.

The combination of high mortgage rates and soaring home prices (which, as we’ll discuss later, are not expected to decrease anytime soon) is creating significant challenges for first-time homebuyers. From July 2023 to June 2024, only 24% of homes purchased were by first-time buyers, marking the lowest level since 1981, according to the National Association of Realtors. For context, prior to 2008, first-time buyers typically accounted for around 40% of all home purchases. What we’re seeing is a shift in preferences among Americans looking to buy their first home, driven largely by the difficulty in meeting the costs of purchasing and financing. Many are opting to delay or postpone their homebuying plans, missing out on the long-term financial benefits of equity growth that traditionally comes with homeownership. For many Americans, this long-term value appreciation has been a key driver of wealth accumulation.

On the macroeconomic front, economists and financial experts warn that Trump’s proposed policies could increase the federal budget deficit by $7.75 trillion over the next decade. To fund this gap, the government will likely need to issue additional bonds, including 10-year Treasury bonds. This, in turn, is expected to push government bond yields higher, which could keep mortgage rates elevated in the short term. However, the Fed’s anticipated rate hikes should help bring mortgage rates down over the medium and long term. We are closely monitoring these developments and will continue to adjust our strategies in response to evolving policy changes.

Turning to the rental market, a recent report by CoStar revealed that the vacancy rate for rental apartments stabilized in the last quarter, after three years of increasing vacancies. While it’s too early to declare a full market reversal, it’s clear that demand for rental properties has surged, reaching its highest level since 2021. Over the past two years, more than 1.2 million new apartment units have been added to the market, all of which were quickly absorbed due to strong demand. If this trend continues and housing prices remain near record highs (and with new construction slowing significantly, there’s no indication of any immediate change), rental prices are likely to continue rising. As a result, apartment owners are expected to retain significant bargaining power, leading to further price increases and higher rents in 2025.

In addition to the rental market, there’s been a noticeable uptick in apartment building sales across the U.S. More and more investors are now concluding that the market has hit its bottom, while sellers are becoming more flexible with their pricing.

In New York City, median rents for new leases saw a notable jump in October after a period of slight declines. Over the past 12 months, the median rent in Manhattan increased by 2.4%, reaching $4,295. A similar trend occurred in Brooklyn and Queens, where the median rent for new leases rose 3.2%, to $3,600, in Brooklyn, and 4.8%, to $3,350, in Queens. This increase in rent is yet another sign that prospective homebuyers are opting to continue renting due to high mortgage rates, which in turn is driving up rental prices.

Regarding home sales, while transaction volume remains lower than the record levels seen in 2021—when interest rates were at historic lows during the COVID-19 pandemic—recent trends indicate a market recovery. October saw a 43% year-over-year increase in contracts signed in Manhattan and Brooklyn, with 1,336 contracts compared to 940 in the same month last year. This upward trajectory has been consistent since July, when the number of signed contracts rose by 35% year-over-year, continuing to climb each month. According to Jonathan Miller, the report’s author, these trends suggest that the market is recovering from its 2023 lows, signaling the beginning of a return to more typical market activity.

An interesting note is that, despite the rise in transactions, the number of apartments available for sale remains virtually unchanged compared to last year, totaling 1,964 properties. This is primarily due to the release of several new projects nearing completion, which are now entering the market as they approach occupancy.

Lastly, we invite you to join us for our annual webinar this December, where we will review the fund’s activities over the past year and share our outlook for the year ahead. An email with the exact dates and registration details will be sent to you shortly.

Erez Britt, Founder and CEO

Example of a recent loan funded:

Vernon Blvd Astoria NY + Drive Astoria NY

Last month, Golden Bridge secured a $28,500,000 loan with a first-position lien to refinance a newly developed rental complex in Astoria Queens located on the riverfront facing Manhattan’s Upper East Side. The complex consists of two adjacent buildings each comprising of 51 residential units, 100 parking spaces and amenities such as laundry rooms, exercise rooms, computer room, conference rooms and outdoor spaces for the residents. At the time of origination, the first building was complete and the second was 90% completed, and 20 of the 102 units were already under contract. Golden Bridge is deeply familiar with the property market in North-West Queens and has been actively involved in financing deals multifamily and residential condominium developments in this area. After conducting thorough due diligence on both the borrower and the property, we structured the loan and its accompanying fees to maximize returns for our investors.

Loan Amount: $ 28,500,000

Property Value (As Is): $ 56,500,000

LTV As Is (loan to property value ratio): 50%

Loan Duration: 9 Months

Reminder that it is possible to see the fund’s loans on New York City’s website:

https://a836-acris.nyc.gov/DS/DocumentsSearch/PartyName

(Business party name: Golden Bridge)

For additional information, don’t hesitate to contact us.